UAE Cabinet Decision No. 34 of 2025 – Key Provisions on Investment Funds and Limited Partnerships

On 27 March 2025, the UAE Cabinet issued Decision No. 34 of 2025 concerning Qualifying Investment Funds (QIFs) and Qualifying Limited Partnerships (QLPs) for the purposes of Federal Decree-Law No. 47 of 2022 on the taxation of corporations and businesses. The Decision, which applies to tax periods beginning on or after 1 January 2025, repeals Cabinet Decision No. 81 of 2023 and introduces updated requirements for entities seeking exemption from corporate tax.

Scope and Definitions

The Decision clarifies several definitions relevant to its application, including Investment Business, Immovable Property Income, and the conditions under which ownership interests and related party considerations affect the tax treatment of investors. These definitions align with the Corporate Tax Law while providing additional context specific to investment structures.

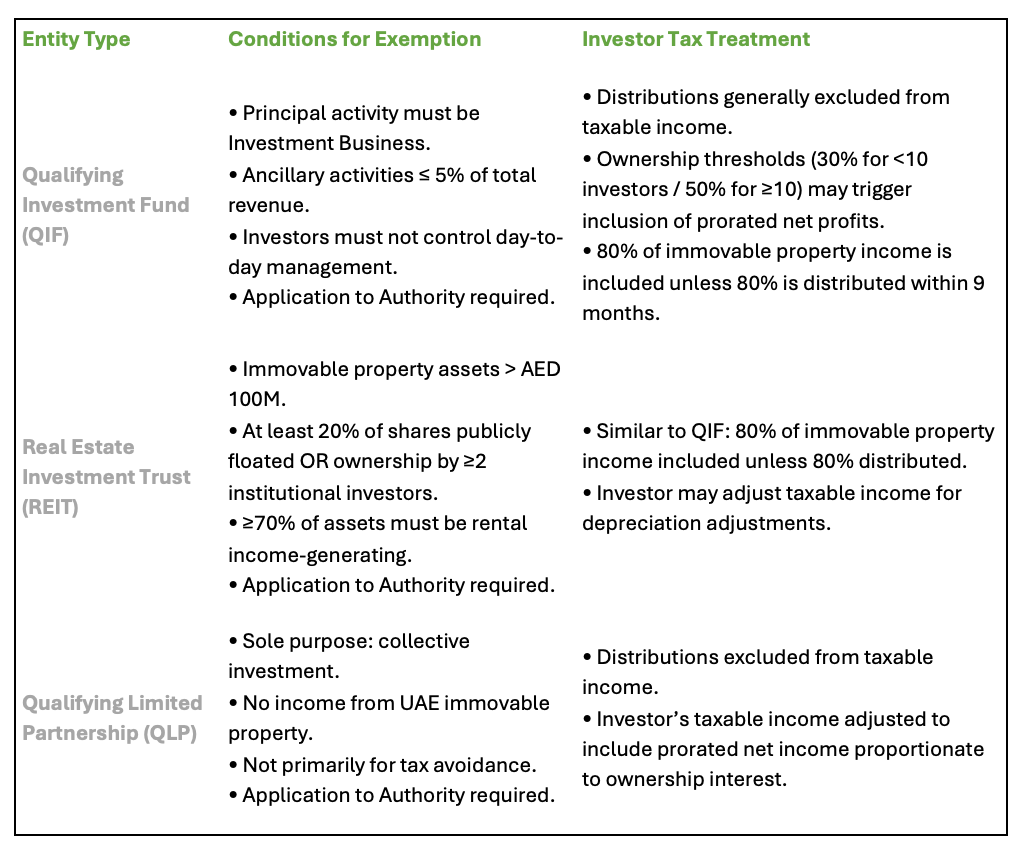

Conditions for Exemption – Qualifying Investment Funds

An investment fund, other than a Real Estate Investment Trust (REIT), may seek exemption from corporate tax where it meets all statutory requirements, including:

- Conducting Investment Business as its principal activity, with other activities being ancillary or incidental.

- Ensuring that investors do not exercise control over its day-to-day management.

- Providing investors with information necessary to calculate their taxable income, as required by law.

The Decision further outlines scenarios in which an investor’s taxable income may be adjusted, particularly where certain thresholds of ownership or influence are reached.

Real Estate Investment Trusts

The Decision establishes specific criteria for REITs to qualify for exemption. These include, among others:

- Maintaining immovable property assets exceeding AED 100 million.

- Meeting ownership or listing requirements (e.g., a public float of at least 20% of shares or ownership by two or more institutional investors).

- Holding at least 70% of assets in rental income-generating property.

The treatment of income distributions and immovable property income is governed by detailed provisions within the Decision.

Qualifying Limited Partnerships “QLP”

A QLP may apply for exemption where:

- Its principal activity is collective investment, and any other activities remain ancillary or incidental.

- It does not derive income from UAE immovable property.

- Its purpose is not primarily to avoid corporate tax.

Entities wholly owned by QLPs may also seek exemption if they exclusively undertake activities related to holding assets or investing funds on behalf of the QLP. The Decision prescribes conditions under which exempt status may be lost, including periods of non-compliance.

Other Provisions

The Decision also addresses unincorporated partnerships, depreciation adjustments, and procedural aspects such as the application process and conditions for maintaining exempt status. Importantly, entities that fail to meet the conditions may lose their exemption for a defined period.

Effective Date

Cabinet Decision No. 34 of 2025 applies to tax periods commencing on or after 1 January 2025. Entities operating within the scope of this Decision should review its provisions in the context of their specific circumstances.

We urge you to review the full cabinet decision here.

For further details please visit the Federal Tax Authority official website.

Disclaimer

Chrysalis monitors developments in UAE corporate tax law to ensure clients remain informed of regulatory changes. While we DO NOT provide legal or tax advice, we assist businesses in understanding the regulatory landscape and connecting with the appropriate professional support when required.

This article is intended solely to provide a general overview of Cabinet Decision No. 34 of 2025. It does not constitute legal or tax advice and should not be relied upon as such. Entities should seek independent professional guidance before taking any action based on this information.

For further information or assistance with UAE Corporate Tax and VAT matters, please contact our Tax Department.

Email: [email protected]

Phone: +971 454 13205

Website: www.chrysalisserve.com

#corporatetaxuae #uaetax #taxlawuae #taxreturn #taxfiling #corporatetaxregistration #taxfile #taxapplication #freezone #taxrate #ministryoffinance #taxlaw #corporateincometax #conductbusiness #emiratelevel #businessesintheuae #taxableprofits #capitalgains #taxreturn #cumentationrequirements #taxableperson #taxcredits #oecdbaseerosionandprofitshifting #taxableincomeaboveaed375,000 #qualifyingpublicbenefitentity #unitedarabemiratesuae #extractivenaturalresourcebusiness.

Want to set up a business in the UAE? Calculate your business setup cost today!