E-Invoicing in the UAE: What Your Business Needs to Know

As the UAE continues its digital transformation, the shift to electronic invoicing (e-invoicing) represents a major step forward for businesses.

The new e-invoicing framework—overseen by the Ministry of Finance (MoF) and the Federal Tax Authority (FTA)—will streamline tax compliance, enhance transparency, and support the UAE’s vision for a fully digital economy.

What is e-invoicing?

At its simplest, e-invoicing means that invoices (and credit notes) are:

- Generated in a structured digital format (not just a PDF or scanned image)

- Exchanged electronically between supplier and buyer via a certified network

- Reported—or made available—to the FTA in near real-time

In the UAE, the designated e-invoicing system is being developed jointly by the MoF and FTA.

An e-invoice is defined as “a structured form of invoice data that is issued and exchanged electronically,” meaning unstructured formats (PDFs, scanned copies, or Word documents) do not qualify.

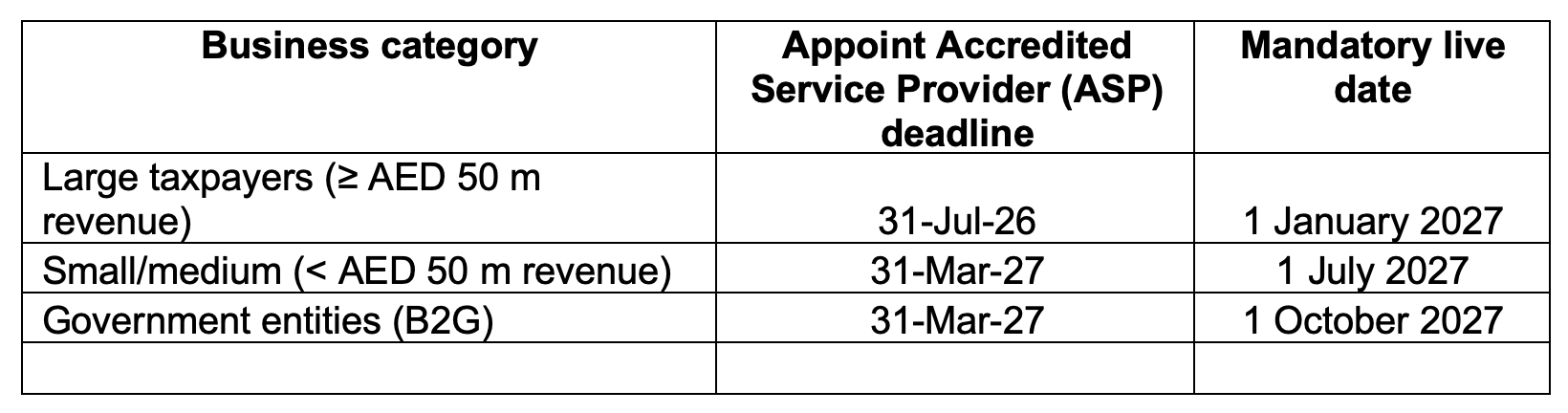

Key Implementation Timeline & Scope

- Businesses should be aware of the following legislative updates and implementation phases:

- Federal Decree-Law No. 16 of 2024 (amending the VAT Law) and Federal Decree-Law No. 17 of 2024 (amending the Tax Procedures Law) establish the legal foundation for e-invoicing.

- The rollout is phased, based on Ministerial Decision No. 243 of 2025 (scope and technical rules) and Ministerial Decision No. 244 of 2025 (implementation timelines).

Summary of deadlines:

Scope:

The e-invoicing mandate applies initially to B2B (business-to-business) and B2G (business-to-government) transactions.

B2C (business-to-consumer) transactions are currently out of scope for the mandatory phase.

Key Technical & Compliance Requirements

To comply, businesses will need to upgrade systems and workflows. The main requirements include:

1. Structured Data Format

Invoices must be issued in structured formats such as XML or JSON, following standards like UBL or Peppol PINT (UAE-specific version).

Traditional PDFs or scanned copies will not be accepted.

2. Use of an Accredited Service Provider (ASP)

All businesses must use an MoF/FTA-accredited ASP.

The ASP validates invoice data, transmits it to the buyer, and reports it to the FTA through the “five-corner model” (issuer’s ASP, receiver’s ASP, buyer, seller, and tax authority).

3. Transmission & Reporting

Invoices must be transmitted and reported through the certified network within the defined timeframe—typically soon after the taxable event.

4. Storage & Archiving

Electronic invoices must be securely stored and accessible in compliance with the Tax Procedures Law.

Retention is generally required for five years, with extensions in special circumstances.

Key Takeaways

- The UAE’s mandatory e-invoicing regime for B2B and B2G transactions begins in January 2027 (large taxpayers first).

- Invoices must use structured data (XML/JSON), an accredited ASP, and secure digital storage.

- Businesses should act now to assess readiness, upgrade systems, and train staff.

- E-invoicing is not just a compliance requirement—it’s a strategic opportunity for digital efficiency.

Disclaimer

This article is for informational purposes only and does not constitute legal or tax advice.

Businesses potentially affected by these changes should seek advice from qualified professionals or consult the Federal Tax Authority (FTA) and Ministry of Finance (MoF) for official guidance.

Contact Our Tax Department:

If you have questions or require assistance regarding UAE Corporate Tax or VAT, our tax professionals are here to help.

Email: [email protected]

[email protected]

Phone: +971 454 13205

+971 457 52971

Website: www.chrysalisserve.com